The Child and Adult Care Food Program (CACFP) budget season is approaching, which means it’s time to plan out your Food Program’s expenses. Every year Sponsors and Center-based programs must submit an annual budget. In addition, they should submit revisions to the budget after periodic analysis and before actual changes in the budget are made.

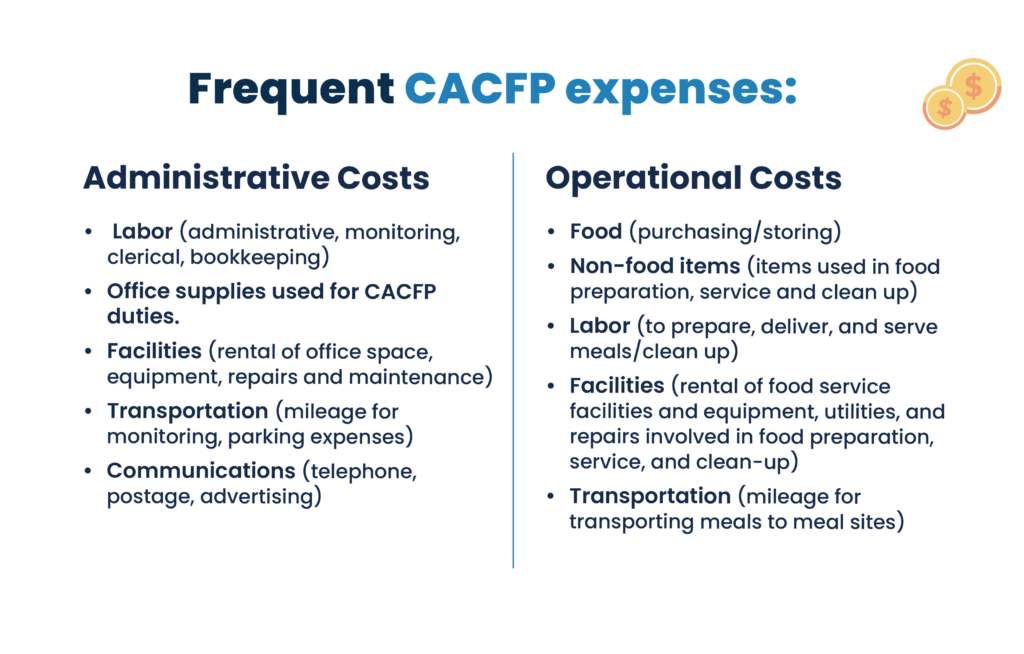

The budget includes two types of allowable costs, direct and indirect costs, which are further categorized into Administrative and Operational Costs. Here are some examples of the frequent CACFP expenses:

Direct costs are incurred specifically for a program or other cost objective and can be readily identified as a particular objective, such as food service. On the other hand, indirect costs are typically incurred for the benefit of multiple programs, functions, or other cost objectives and, therefore, cannot be readily or specifically identified with a particular program or other cost objective.

Also, direct costs are easily identified and assigned to the CACFP. However, indirect costs cannot be easily identified or assigned to the CACFP.

Direct costs are costs incurred specifically for a program or other cost objective, and can be readily identified to a particular objective, such as food service.

Example: Food, wages/salaries of staff working solely in the food service.

Indirect costs are costs typically incurred for the benefit of multiple programs, functions, or other cost objectives, and therefore cannot be readily or specifically identified with a particular program or other cost objective.

Example: Administrative overhead (may include, but not limited to, fringe benefits, accounting, payroll, purchasing, facilities management, utilities).

Only the share of costs that benefit the CACFP can be assigned to the CACFP. If the Sponsors and Center-based programs claim indirect costs, the rate must be part of their cost allocation plan. A cost allocation plan is a written explanation of how costs are classified.

Administrative costs are allowable expenses related to planning, organizing and managing a food service under CACFP, and allowed by the state.

Example: Salaries, wages, and fringe benefits for staff that approve income eligibility forms, provide training, and monitor sites.

Operating costs are allowable expenses for serving meals to eligible participants in eligible sites.

Example: Food, nonfood supplies, foodservice equipment.

Administrative and operating costs can be either direct or indirect costs

“According to the Food & Nutrition Service (FNS), the phrase “prior approval” is used to identify costs that must be specifically identified by item and amount during the budget submission process to permit the State agency to fulfill the regulatory requirements.”

According to the Budgets A Child and Adult Care Food Program Handbook some expenses require specific prior written approval. Some examples of costs requiring specific prior written approval are:

Remember to refer to the budget all year long for the following different reasons:

If an item is not included in the approved budget, you will need to submit a budget revision to include the item in the budget. The cost may not be incurred prior to the approval of the budget revision.

* Please contact your sponsors or agency for more information.

* Please contact your sponsors or agency for more information.

Resources:

Guidance for Management Plans and Budgets A Child and Adult Care Food Program Handbook

CACFP Training Texas

References:

Oregon Department of Education, Child Nutrition Programs training.